We have to speak. Extra particularly, we have to discuss one of the crucial frequent myths I see making its manner across the private finance world. That fable is:

“Renting is a waste of cash.”

A number of instances per week, I hear from individuals who need to purchase a house as a result of they’re fearful they’re throwing away cash by renting. Perhaps they heard this from their mother and father, or perhaps it was strangers on the web.

However wherever they heard it, they made a significant monetary resolution based mostly on different individuals’s choices moderately than what’s really greatest for his or her state of affairs.

On this article, I need to clear up that false impression by displaying you ways renting is unquestionably not throwing away cash.

Why individuals say that renting is a waste of cash

Earlier than I discuss why renting is unquestionably not throwing away cash, let’s cowl the explanation why individuals assume that is the case. As a result of within the curiosity of full disclosure, there are some advantages of homeownership which have made it so well-liked.

1. YOUR MORTGAGE BUILDS EQUITY IN YOUR HOME

Each month once you pay your mortgage, a portion of your fee goes towards your principal (that means the quantity you initially borrowed).

Your fairness is the distinction between your private home’s worth and the principal you continue to owe in your mortgage. And so, as you pay down your principal, your fairness within the residence will increase.

2. HOMEOWNERS BENEFIT FROM RISING HOME VALUES

The true property market might ebb and movement, however similar to the inventory market, residence values usually improve over time. In consequence, many householders are in a position to promote their properties for greater than they paid for them, leading to a capital achieve.

I’m not going to argue the validity of both of those statements. It’s completely true that paying your mortgage builds fairness in your house and that your private home’s worth is more likely to rise through the years. However within the subsequent couple of sections, we’ll discuss why these issues don’t matter as a lot as you would possibly assume.

The return on funding of homeownership

It’s true that residence values have constantly elevated through the years. Since 1940, residence values have elevated a mean of 5.5% per 12 months.

Relying in your investing expertise, you would possibly assume 5.5% sounds fairly good. However what about once you examine it to different investments?

In line with the Securities and Trade Fee, the inventory market sees a mean annual return of about 10% per 12 months. That’s almost twice as a lot as the rise within the worth of a house. And shares don’t include the upkeep prices required of homeownership, as we’ll talk about later.

SO, JUST HOW DIFFERENT ARE THOSE PERCENTAGES?

Let’s say you invested $100 per thirty days for 30 years into an funding with a 5.5% annual return. After 30 years, you’d have greater than $87,000.

However in case you had invested that very same $100 per thirty days into an funding WITH a ten% return? Due to compound curiosity, you’d find yourself with simply shy of $200,000 — greater than twice the return on a 5.5% funding.

It’s additionally necessary to notice that the quantity you pay for a home is way from the one funding you make into it. While you account for all the opposite bills, it’s possible your returns from the rise in worth are fully worn out.

Let’s do the mathematics: Renting vs. shopping for

It’s simple to assume you’re throwing away cash by renting as a result of the cash you pay every month doesn’t construct fairness in your house. However let’s have a look at an instance which may change your thoughts.

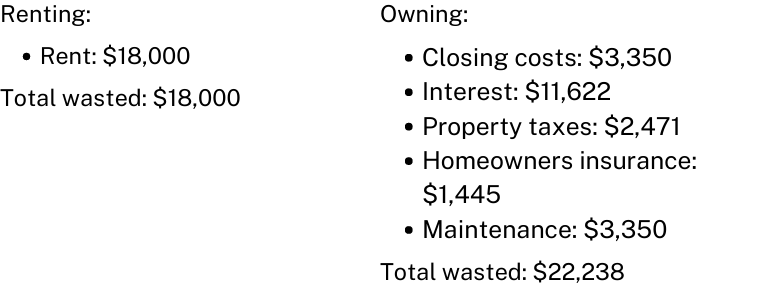

CLOSING COSTS

Closing prices aren’t an ongoing expense of homeownership, however they make up a considerable price within the first 12 months. Closing prices run between 1% and three% of the house’s buy value. For a house priced at $335,000, your closing prices can be $3,350.

INTEREST

Let’s say you lease an house for $1,500 per thirty days. You’re sick of throwing away cash renting, so you purchase that $335,000 residence with a month-to-month mortgage fee of $1,500.

However that total $1,500 doesn’t construct fairness in your house. In actual fact, within the early years of homeownership, most of your month-to-month fee goes towards curiosity. If you are interested price of three.5%, then about $11,622 of your fee goes towards curiosity within the first 12 months.

Observe: I discovered these numbers utilizing Bankrate’s mortgage amortization calculator for a mortgage of $335,000 and an rate of interest of three.5%.

PROPERTY TAXES

Subsequent, let’s discuss property taxes. Charges differ relying on the place you reside. However in line with the U.S. Census Bureau, the typical family spends about $2,471 on property taxes every year. We’ll use that for the needs of this instance.

HOMEOWNERS INSURANCE

One other ongoing price of homeownership is owners insurance coverage. The fee will differ relying on the place you reside, the scale of your private home, how a lot protection you need, and plenty of extra elements. In line with ValuePenguin, the typical price of householders insurance coverage is $1,445 per 12 months.

MAINTENANCE

Lastly, let’s discuss residence upkeep. As a home-owner, you’re chargeable for any repairs that must be carried out. There’s no extra landlord to name.

Sadly, it’s not possible to foretell how a lot you’ll spend on upkeep every year. Nevertheless, consultants suggest planning for about 1% of the price of your private home. In your $335,000 residence, you would anticipate to spend $3,335.

RENTING VS. BUYING: WHAT’S THE VERDICT?

Individuals prefer to argue that renting is throwing away cash. However as you’ll be able to see, there are a lot of bills of homeownership that don’t construct your fairness within the residence. Let’s examine how a lot cash you throw away renting versus in your first 12 months of homeownership.

As you’ll be able to see, you “throw away” considerably extra in your first 12 months of homeownership than you’ll be renting. And positive, closing prices are a one-time price moderately than an ongoing one. However even in case you get rid of that price, you continue to throw away extra money per 12 months proudly owning a house than you do renting.

Proudly owning a house vs. actual property investing

None of that is to say which you can’t make cash from actual property investing. In actual fact, It’s necessary actual property might be extremely worthwhile. However your main residence is just not an funding property.

While you buy an funding property, the growing residence worth isn’t actually the place you make your cash. You make your cash by renting out the property and bringing in passive revenue every month.

In different circumstances, you can also make cash by flipping properties, the place you purchase a house, renovate it, after which it for a big revenue. Neither of those conditions applies to your private home.

Is renting higher than shopping for?

You is perhaps studying this text and considering that I’m saying homeownership is a nasty thought or a waste of cash. However that’s not remotely true. In actual fact, my husband and I are saving for a house proper now.

We need to personal a house as a result of we love our group, and we need to grow to be a extra everlasting a part of it. We wish an area that’s really ours. We wish a yard the place our canine can run round and the place we are able to entertain buddies.

Since I initially wrote this publish, my husband and I purchased a house. Shopping for comes with an enormous price ticket and plenty of accountability, however we’ve discovered it price it, even with out the monetary achieve.

There are additionally many causes I really like renting a house. I really like that I don’t should mow the garden in the summertime or shovel the snow within the winter. I really like that if an equipment breaks down, my landlord replaces it. I really like that if I need to transfer, I can accomplish that with little or no discover as a result of I don’t should promote a home first.

There are a lot of nice causes to personal a house, and there are a lot of nice causes to lease. However the advantages of homeownership aren’t monetary.

Last Ideas

We’ve all heard the monetary fable that renting is throwing away cash. And whereas there are a lot of nice causes to personal a house, considering that you simply’re saving cash isn’t considered one of them. In actual fact, as we found out above, you really throw away much more cash by proudly owning a house.

{kind=link}